Why Should You Consider the Deferred Sales Trust?

If you are considering the sale of a business, corporation, or investment real estate, you may face capital gains tax associated with that sale. For the investor who does not want to continue holding investment property or remain in the same business, a Deferred Sales Trust should be considered. According to Section 453 of the Internal Revenue Code, the Deferred Sales Trust provides investors a solution whereby they can defer capital gains upon the sale of their assets and redirect the sale proceeds into cash or whatever types of investments suit their needs, income requirements and objectives.

What is a Deferred Sales Trust?

The Deferred Sales Trust is a legal contract between you and a third-party trust in which you sell real property, personal property or a business to the Deferred Sales Trust created for you. This is in exchange for the Deferred Sales Trust’s contractual promise to pay you a certain amount over a predetermined future period of time in the form of an installment sale note or promissory note. It is often referred to as a “self-directed note” because it is usually in the Trust’s interest to agree to terms that allign with the Sellers needs and objectives. (of course, per IRS rules the terms of the note should be ‘reasonable’ given the circumstances of a typical arms length transaction)

The Deferred Sales Trust gives you the ability to control your capital gains tax exposure, reinvestment terms of the sales proceeds, and installment payments made from the trust.

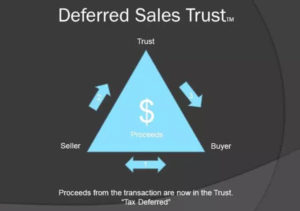

How Does a Deferred Sales Trust Work?

The process begins when a property or business owner transfers their asset to a trust managed by a third-party company, as Trustee on their behalf. The third-party company acts as trustee over the asset, and the owner is the secured creditor of the trust that holds the asset. The trust will sell the asset to the owner’s buyer and manage and distribute the sale proceeds of the trust according to an agreed-upon installment contract that the owner sets up ahead of time with the Trustee.

The sales proceeds can be held in cash, reinvested and distributed according to the direction of the owner’s installment contract with the Trust. There are zero taxes to the trust on the sale, since the trust purchases the property from the owner for the same price for which it is sold.

The tax code does not require payment of any of the capital gains taxes until an investor starts receiving installment payments that include principal. The owner is then able to control if, when, and how there will be capital gains tax exposure over the installment contract period by negotiating the installment contract in accordace with their objectives.

The installment contract between the owner and the trust company provides flexible options on when and how payments can be made. Initially, the owner may have other income and may not need the installment payments right away, which would defer income and capital gains taxes. If an owner wants income but does not want to pay capital gains taxes, he/she can set up the installment contract to pay partial or full interest-only payments from the reinvested sales proceeds. According to IRC Section 453, this strategy can defer the capital gains tax indefinitely.

Legal, Tested, Proven

Highlights of the legal viability of the DST include:

- The DST is a proprietary strategy developed by our tax attorneys over 27 years ago

- Successfully transacted over 4,000 DST transactions totaling hundreds of billions of dollars

- 16 field audits by the IRS all resulting in “No-Change” Letters

- Formal IRS review with The Estate Planning Team and our Tax Attorney – No adverse findings

- Reviewed by FINRA and SEC with no adverse opinion – Allows broker-dealers to approve their advisors to participate in the DST Strategy for clients.

- The Estate Planning Team and our Tax Attorney provide Audit Defense at no extra cost

- Also, when clients are trying to research on their own, the basis for the DST is IRC 453 dealing with Installment contracts.

If you would like to schedule a call or video conference with Greg Reese, one of the leading DST Trustees in the country, you can use the following link to his calendar https://calendly.com/reefpoint-team, or call Greg at (866) 867-8633.